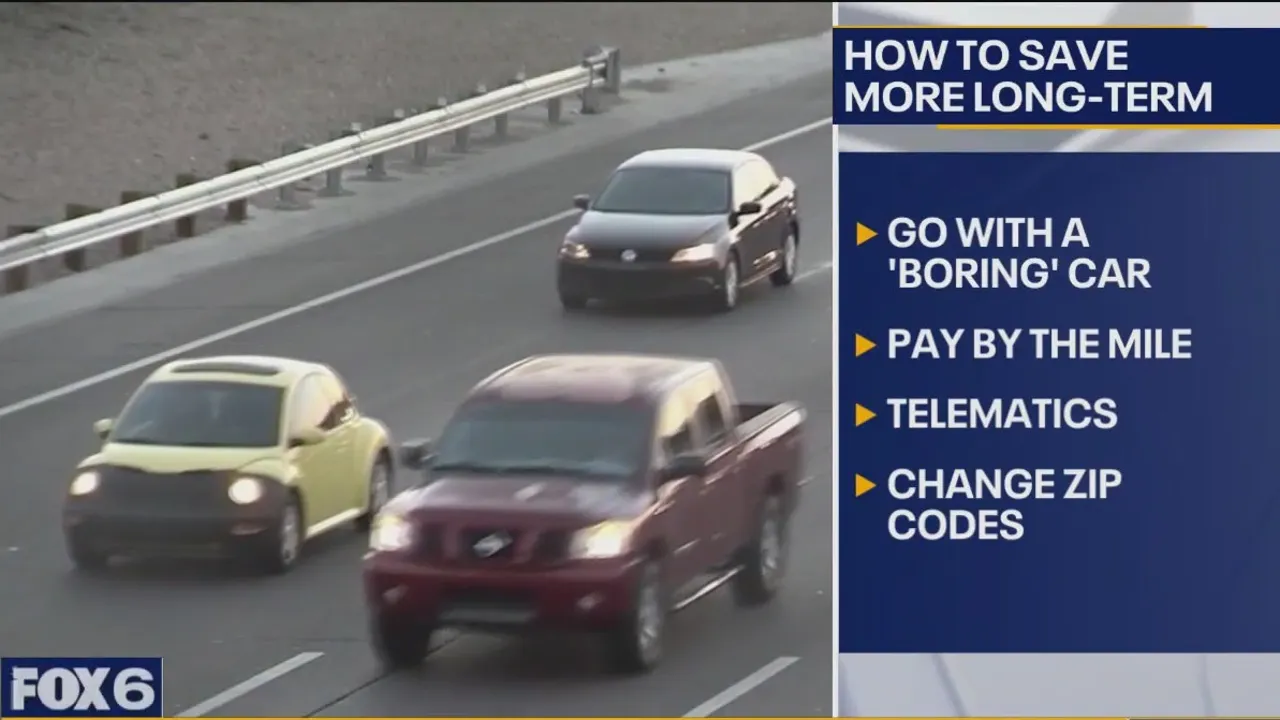

Adequate car insurance: Finance professor shares ways to save

How did your country report this? Share your view in the comments.

Diverging Reports Breakdown

3 ways to know if your 401(k) is too aggressive

A 401(k) retirement plan is one of the most popular ways to save money for retirement. Aggressive portfolios have a high exposure to stocks and stock funds, making them more volatile over the short term. To reduce risk, investors can add more bond funds to their portfolio or even hold some CDs. If you think your portfolio might be too aggressive, here are some signs to look for: Your account balance fluctuates a lot and you worry a lot about downturns in your 401(K) If someone tends to move out of their investments because of volatility, then the portfolio is probably too aggressive for them, says Randy Carver, president and CEO of Carver Financial Services in the Cleveland area.. If they are not invested enough to meet their long-term needs, it is too conservative, says Matthew Trujillo, CFP at Center for Financial Planning in Southfield, Michigan. It can make a lot of sense if you have a long time until retirement, but it can really sink you financially if you need the money in less than five years.

What you can do if your portfolio is too aggressive

A 401(k) retirement plan is one of the most popular ways to save money for retirement and score some tax breaks for doing so. But often these plans don’t provide a lot of guidance on how to manage them, and participants end up with wildly aggressive portfolios, or, what experts often see, a portfolio so conservative that it barely budges year after year.

Here’s how to see if your 401(k) is too aggressive and, if so, some steps you can take to fix it.

Key takeaways Aggressive portfolios have a high exposure to stocks and stock funds, making them more volatile over the short term.

Retirement investors need to balance their need for growth and their need for stability.

Those who are nearing retirement and who need to tap their 401(k) should be extra careful with their investment allocations.

What is an aggressive 401(k) investment?

When financial advisors speak of having an aggressive 401(k), they generally mean how much of your assets are in stocks or stock funds. Stocks are an attractive long-term investment, but they fluctuate a lot in the short term. That’s problematic, especially for soon-to-retire investors. If all or almost all of your retirement account is in stocks or stock funds, it’s aggressive.

While having a more aggressive 401(k) can make a lot of sense if you have a long time until retirement, it can really sink you financially if you need the money in less than five years. To reduce risk, investors can add more bond funds to their portfolio or even hold some CDs.

How the market can affect an aggressive 401(k) strategy

“A large downturn in the market immediately preceding retirement can have devastating effects on an individual’s standard of living in retirement,” says Dr. Robert Johnson, finance professor at Creighton University’s Heider College of Business.

Johnson points to those who retired at the end of 2008 and who were invested only in the Standard & Poor’s 500 Index (S&P 500), which contains hundreds of top companies. “If they were invested in the S&P 500, they would have seen their assets fall by 37 percent in one year,” he says.

But those who had some investments in other assets such as bonds or even cash would have seen a much lower overall decline. Of course, any money in the S&P 500 would have declined with that index, but by having fewer eggs in that basket, their overall portfolio declined less.

That principle of diversification is paramount in making sure that your portfolio is not too aggressive.

But many workers make the opposite mistake, not investing aggressively enough. If you have more than five years until retirement, and certainly if you have 10 or more, you can afford to be more aggressive, because you have the time to ride out the market’s ups and downs.

3 signs your 401(k) is too aggressive

If you think your portfolio might be too aggressive, here are some signs to look for:

1. Your account balance fluctuates a lot

It can be exciting to see your balance run up quickly, but it’s important to realize that this could be an effect of a 401(k) that’s invested too heavily in stock funds and not enough in safer alternatives.

“If you take someone with an account balance of $100,000 and after one month their account is now $110,000, or 10 percent growth in a month, what that tells me is that they probably have most of their money in stocks,” says Matthew Trujillo, CFP at Center for Financial Planning in Southfield, Michigan.

“This will feel great when things are going up, but that investor needs to be prepared to see some significant paper losses when we experience a downturn,” says Trujillo.

2. You worry a lot about your 401(k)

If downturns in your 401(k) cause you a lot of worry, then you may be investing too aggressively.

“If someone tends to move out of their investments because of volatility, then the portfolio is probably too aggressive for them,” says Randy Carver, president and CEO at Carver Financial Services in the Cleveland area.

But it’s key to understand that while stocks are more volatile and you may not always feel comfortable owning them, they are also one of the best ways to grow your wealth over time, even with high interest rates and historically high bond yields.

“If they are not invested to grow enough to meet long-term needs, it is too conservative,” says Trujillo. “The key is to look at longer periods of time, two or three years or more, to see trends, not just one or two months.”

3. You need cash soon, but your 401(k) doesn’t have any

If you know you’re going to need cash in the next few years, your 401(k) needs to factor that in. That doesn’t mean you need to sell everything and go to cash now, but you can leave new contributions in cash or move them into lower-risk bond funds, slowly reducing aggressiveness.

To gauge your plan’s aggressiveness, use the rule of 100, suggests Chris Keller, partner at Kingman Financial Group in San Antonio. With this rule, you subtract your age from 100 to find your allocation to stock funds. For example, a 30-year-old would put 70 percent of a 401(k) in stocks. Naturally, this rule moves the 401(k) to become less risky as you approach retirement.

Pointing to the importance of a 70-year-old reducing risk, Keller says, “Losing half of your portfolio while at this age might have a huge impact on what your retirement looks like.”

Invest Search Icon Need an advisor to help you set your goals? Need expert guidance when it comes to managing your investments or planning for retirement? Bankrate’s AdvisorMatch can connect you to a CFP® professional to help you achieve your financial goals.

How aggressive should your 401(k) be?

Many financial advisors say that investors with decades until retirement could reasonably invest 100 percent of their 401(k) into diversified stock funds. Others with less than a decade until they need the money may consider becoming more conservative over time.

How aggressively you need to invest depends on many factors, but here are some of the most important for determining how to invest:

Future needs. If you need a lot of money for retirement or want to live an opulent lifestyle, you should invest more aggressively. If your needs are lower, you can afford to be less aggressive.

If you need a lot of money for retirement or want to live an opulent lifestyle, you should invest more aggressively. If your needs are lower, you can afford to be less aggressive. Ability to save. If you have a strong ability to save money, then you can afford to take less risk and still meet your financial goals. If you can’t save as much, then you’ll need to be more aggressive with your investments to reach your goals.

If you have a strong ability to save money, then you can afford to take less risk and still meet your financial goals. If you can’t save as much, then you’ll need to be more aggressive with your investments to reach your goals. Time horizon. The more time until you need the money, the less aggressively you need to invest. If you have decades until retirement – even just a full decade – you have a lot of time to ride out the market’s fluctuations and take advantage of the compounding power of stocks.

The more time until you need the money, the less aggressively you need to invest. If you have decades until retirement – even just a full decade – you have a lot of time to ride out the market’s fluctuations and take advantage of the compounding power of stocks. Risk tolerance. If you have low tolerance for risk, you may not want to be so aggressive, but that means you’ll need to save more or give yourself more time before retirement to accumulate the level of money that you need.

Those are some of the key factors to consider when determining how aggressively to invest.

What is the average return for an aggressive 401(k)?

There’s no hard and fast rule for what you can earn on an aggressive portfolio. The return always depends on the performance of the stocks or stock funds in the portfolio. Stocks can fluctuate a lot, but historically a broadly diversified portfolio of stocks has shown strong gains.

For example, the Standard & Poor’s 500 index has returned about 10 percent annually. The best mutual funds have done even better recently, with some topping over 20 percent annually.

But that’s the level of return you can achieve only if you’re fully invested in the most aggressive kind of portfolio — all stocks. If you need a portion of your portfolio to be more conservative, perhaps because you’re nearing retirement, you’ll probably want to add safer but lower-yielding bonds to the mix. In that case you should expect your overall returns to be lower.

And it’s worth repeating that stocks fluctuate, so you have to hold on or you won’t get these returns. Actively trading generally leads to significant underperformance, compared to investing passively.

Disadvantages of having a too aggressive 401(k) portfolio

Having a 401(k) portfolio that’s too aggressive can come with a number of disadvantages, from the annoying to the financially destructive. Here are some of the most common:

Your wealth fluctuates a lot. If you’re overexposed to stocks, your portfolio will bounce around more than it will with less exposure. That can be OK if you have a long time until retirement, but it’s potentially much more costly if you’re close to retirement.

If you’re overexposed to stocks, your portfolio will bounce around more than it will with less exposure. That can be OK if you have a long time until retirement, but it’s potentially much more costly if you’re close to retirement. You may need to access your money when the market’s down. If you’re too aggressive with only a few years or less until retirement, you’re wagering that the market will stay strong until you tap your money. If it doesn’t, you may have to start taking distributions in a down market, hurting your long-term retirement finances.

If you’re too aggressive with only a few years or less until retirement, you’re wagering that the market will stay strong until you tap your money. If it doesn’t, you may have to start taking distributions in a down market, hurting your long-term retirement finances. A too-aggressive portfolio may scare you out of the market. The secret to scoring big returns in the market is staying invested. So if a volatile portfolio scares you out of the market, you lose the key advantage of investing in stocks.

The secret to scoring big returns in the market is staying invested. So if a volatile portfolio scares you out of the market, you lose the key advantage of investing in stocks. Less diversification may mean higher risk. A diversified stock portfolio can be useful, but if you’re in all stocks, your overall portfolio may not be as diversified as it could be. So, if something negatively impacts stocks as a whole, your diversification among stocks won’t help you.

A diversified stock portfolio can be useful, but if you’re in all stocks, your overall portfolio may not be as diversified as it could be. So, if something negatively impacts stocks as a whole, your diversification among stocks won’t help you. If your portfolio is all stock, then you might not generate much cash. If you’re taking distributions, it can be useful to have a portfolio with some cash-producing bonds or CDs, helping you weather a downturn or allowing you to stay invested in stocks, which usually show better long-term returns.

Those are some of the largest disadvantages of being too aggressive in your 401(k).

What you can do if your portfolio is too aggressive

Investors who find their portfolio is too aggressive have potential fixes for this issue that range from simple one-time moves to an overhaul of your financial plan with a financial advisor.

Reduce the risk in your portfolio. The first step is to take down the risk in your portfolio by moving some exposure in stock funds (or even riskier options) into bond funds or even cash, depending on when you need the money.

The first step is to take down the risk in your portfolio by moving some exposure in stock funds (or even riskier options) into bond funds or even cash, depending on when you need the money. Match your portfolio to your temperament. Find an asset allocation between stocks, bonds and cash that meets your needs and temperament. A more aggressive allocation might have 70 percent or more in stocks, while a more conservative one might have that much in bonds. Then stick with this allocation and rebalance it when it moves too far away from your target allocation.“This means that often a market correction is a good time to shift more to stocks, not less,” says Carver. “The key is sticking with a target allocation which eliminates the need to make decisions based on market behavior or predictions.”

Find an asset allocation between stocks, bonds and cash that meets your needs and temperament. A more aggressive allocation might have 70 percent or more in stocks, while a more conservative one might have that much in bonds. Then stick with this allocation and rebalance it when it moves too far away from your target allocation.“This means that often a market correction is a good time to shift more to stocks, not less,” says Carver. “The key is sticking with a target allocation which eliminates the need to make decisions based on market behavior or predictions.” Start reducing risk slowly and before you need it. If you’re managing the portfolio yourself, Johnson recommends starting the risk reduction perhaps as much as five years before you want to access the portfolio. That doesn’t mean you need to go all cash and bonds, but rather gradually move the portfolio toward lower total risk.

If you’re managing the portfolio yourself, Johnson recommends starting the risk reduction perhaps as much as five years before you want to access the portfolio. That doesn’t mean you need to go all cash and bonds, but rather gradually move the portfolio toward lower total risk. Consider a target-date fund. If you don’t want to make these changes yourself, then use a target-date fund to manage the process for you. It automatically shifts money from stocks to bonds as you near your target date, which may be retirement, but could be any time when you need to start withdrawing some cash.

If you don’t want to make these changes yourself, then use a target-date fund to manage the process for you. It automatically shifts money from stocks to bonds as you near your target date, which may be retirement, but could be any time when you need to start withdrawing some cash. Meet with your financial advisor. Meet with your own advisor and your company’s 401(k) advisor each January, says Paul Miller, managing partner at accountancy Miller & Co. in the New York City area.“It’s critical for an employee to hear what they have to say,” says Miller. “Take notes and then go to the web and read reviews about each fund. For example, you can use Morningstar to independently rate and review your funds.”

Meet with your own advisor and your company’s 401(k) advisor each January, says Paul Miller, managing partner at accountancy Miller & Co. in the New York City area.“It’s critical for an employee to hear what they have to say,” says Miller. “Take notes and then go to the web and read reviews about each fund. For example, you can use Morningstar to independently rate and review your funds.” Have your advisor review your 401(k). Finally, it can be useful to have a financial advisor review your 401(k), but you must find one who works in your best interest and not one who is paid to put you in certain financial products. Here’s how to find the right advisor for you.

FAQs

What is an example of an aggressive 401(k) strategy? Caret Down Icon An aggressive investment strategy involves using only high-risk, high-return assets such as stocks or stock funds in your 401(k). Stock funds can deliver among the best returns over time, but they’re more volatile over shorter periods of time. An aggressive fund may be appropriate for an investor with a long time to invest the money, but those with less than a few years until they need the money should take a more conservative approach.

How aggressive should my 401(k) be at age 50? Caret Down Icon If you won’t tap your retirement funds for 12–15 years or maybe more, you have a long time to let your money grow, so you can be relatively aggressive with investing. Some advisors use the Rule of 100 or the Rule of 120 to judge the correct allocation of stocks. To find your percentage allocation to stocks, you subtract your age from 120. So if you’re 50 now, the rule suggests that your allocation to stocks should be 70 percent. As you age, your allocation to stocks declines and your exposure to bonds rises, giving you a more conservative portfolio and more cash income from bonds.

What is the most aggressive investment strategy? Caret Down Icon Any portfolio that is 100 percent allocated to stocks is considered aggressive. Some investors try to make up for lost time by choosing more aggressive investments in a 401(k) right up until they retire. This approach runs a serious risk that the money may not be there when you need to tap it, if the market hits a downturn right before you retire.

Bottom line

“It’s important to note that a retirement date is not the finish line – even if someone is going to retire at age 60 or 65 the funds could be needed for another 20-25 years,” says Carver. “They should continue to be invested in a diversified allocation that has growth potential.”

So even as you age and take a less aggressive investment approach, it’s vital to remember that you probably still need some exposure to stocks in your portfolio and to plan accordingly.

Editorial Disclaimer: All investors are advised to conduct their own independent research into investment strategies before making an investment decision. In addition, investors are advised that past investment product performance is no guarantee of future price appreciation.

14 financial advisers reveal how you should invest $50K right now

The best way to spend $50K depends on your time horizon, risk tolerance and financial goals. Financial advisers can match you to a fiduciary financial adviser, as well as resources like NAPFA and the CFP Board. With the market having come in a bit, this is a great time to put money to work, experts say. The best investments are low-cost, tax-efficient investment vehicles such passively managed index funds and exchange traded funds (ETFs), they say. It’s best to start with a rainy day fund, and if you need access to the funds in the short-term, you might consider a savings account or CD (see some of the best savings account rates here, and CD rates here from our partner Bankrate). If you don’t have an emergency fund, build one. If you have a long-term investment horizon, consider equities and other options — which a financial adviser may be able to help you suss out. It’s better to start by excluding certain companies based on a value-screening criteria.

One thing we all should consider when we have extra money is the time horizon when we’ll need the money, pros told us. If you don’t have an emergency fund, build one — and if you need access to the funds in the short-term, you might consider a savings account or CD (see some of the best savings account rates here, and CD rates here, from our partner Bankrate).

But if your time horizon is longer, you might consider equities and other options — which a financial adviser may be able to help you suss out. (You can use this free tool from our partner SmartAsset that can match you to a fiduciary financial adviser, as well as resources like NAPFA and the CFP Board.)

Here’s how finance pros — everyone from certified financial planners to a finance professor — say they’d invest $50,000 right now.

Bridget Grimes, CFP and president of WealthChoice

“If I had $50K to invest right now and the goal was to fund something in the future (retirement, maybe a home down the road), I would invest in a low-cost, tax-efficient, diversified portfolio of investments. This would be ETFs in a mix of asset classes. With the market having come in a bit, this is a great time to put money to work.”

Jing Zheng, CFP, enrolled IRS agent, MBA and founder of Neat Financial Planning

“First, before making any investment decisions, I always recommend reviewing your cash flow and setting up a solid rainy day fund. Then, I’d recommend allocating 50% to quality large-cap ETF (30%) and small-cap stocks ETF (20%), 40% to short-term Treasuries, and 10% to alternative funds such as hedged equity ETFs to help manage volatility … Consider allocating a reasonable portion of your portfolio to the technology sector, small-cap growth, real estate, and Treasury Inflation-Protected Securities (TIPS) to capture long-term growth while also hedging against inflation.”

Grace Yung, CFP and founder of Midtown Financial Group

“I have been laddering buffered strategies for my clients. These are 15-month stock option strategies that allow for participation in the market on the upside, but are capped at various levels with downside protection anywhere from 10%, 20% and 30% buffers.”

Lance Dobler, CFP, vice president and senior regional director at TIAA

“In general: short-term investors should focus on lower risk, liquid investments such as high-yield savings accounts, short-term bonds, and money market funds to prioritize safety. Longer-term investors should consider a mix of stocks, bonds, and real assets to maximize the potential for growth … Prioritize the use of low-cost, tax-efficient investment vehicles such passively managed index funds and exchange traded funds (ETFs).”

You can use this free tool from our partner SmartAsset that can match you to a fiduciary financial adviser, as well as resources like NAPFA and the CFP Board.

Leo Marte, a CFP from Abundant Advisors in North Carolina

“If I had $50K, I would invest it in mutual funds aligned to my faith values that make a positive impact on the world. These funds start by excluding certain companies based on a value-screening criteria. Through these funds, I have the ability to have a positive impact by investing in businesses that create products and follow practices I personally believe in.”

Charles Sachs, CFP and chief investment officer of Kaufman Rossin Wealth, LLC

“My general thought is that consensus capital market assumptions for stocks over the next 10 years are much lower than the 9% historical return. I’d probably go with a well-diversified private credit fund that is returning in the 9% range and without the market risk associated with stocks and can generate income if needed or, if not, be reinvested.”

Ben Loughery CFP, and chartered retirement planning counselor at Lock Wealth Management

“The best way to spend $50K depends on your time horizon, risk tolerance, and financial goals. Questions that you can ask yourself are do I need this money within one to three years — and if the answer is yes, then prioritize investing in safer assets,” he says. He notes that “safer assets would be high yield savings accounts which currently pay between 4-5% in interest annually. Treasury bills also would be safer assets along with investment grade bonds.”

Are you investing for 5+ years? If that answer is yes, focus more on long-term growth strategies,” he adds. “For long term growth strategies, investing in equities such as the large cap value and large cap growth categories would be an example.”

Robert R. Johnson, professor of finance at Creighton University

“If you have a long-time horizon and want to build wealth then you should put the entire $50K in a passive ETF or mutual fund that tracks a broad index like the S&P 500,” he says, adding that passive investing minimizes fees. “The deleterious effects of high fees and transaction costs also compound over time.”

David Johnston, CFP and managing partner at Amwell Ridge Wealth Management

First, make sure “you have at least six months’ worth of expenses in a readily accessible cash account,” he says. If you need the money “within the next 2–3 years, equities should be off the table. Instead, reinforcing their cash reserves, money market funds, or short-term bonds will likely be more appropriate.”

Andrew Latham, CFP and director of content at SuperMoney

“If you need the money in 1-3 years, keep it safe in a high-yield savings account (4-5% APY), CDs, or treasury bonds. If you have a longer timeline, go for stocks, ETFs, and real estate to maximize growth. Historically, the S&P 500 averages about 10% per year, meaning $50K could grow to over $540K in 25 years if left untouched.

You can use this free tool from our partner SmartAsset that can match you to a fiduciary financial adviser, as well as resources like NAPFA and the CFP Board.

A smart, diversified portfolio might look like this: $30K (60%) in stock index funds, $10K (20%) in bonds or treasuries, $5K (10%) in REITs (real estate investment trusts), and $5K (10%) in high-yield savings for flexibility.”

Michael Hoyle CFP and certified private wealth adviser at Conrad Siegel

“Before you invest, you want to consider the purpose or goal for the money. Do you have a short-term goal like a down payment on a home that you’re saving toward, or is this money to help you build wealth for the future?

Don’t try to time the market – it’s time in the market rather than timing the market that matters. Keeping cash on the sideline while you watch the market climb, waiting for that perfect buying opportunity can be costly.

Focus on what you can control – your asset allocation and level of diversification. The best asset allocation is the one you are comfortable with and can stick with throughout all market conditions.”

Kelsey Wilson, CFP and founder of wealth management firm BlackLines Financial

“The first thing you’re going to want to do is open up an investment account … You can put the money inside of an individual investment account, you can put that money into an IRA, you can put that money into an annuity,” he says. Then pick investments: “The investments will be associated with the timeframe of when you need the money, then that will be broken down based upon whether you’re doing stocks, bonds, or being more conservative.”

Otto Rivera, CFP at White Lighthouse Investment Management

“If I had $50,000 to invest at this moment, I would contribute $19,000 to a tax-advantaged ABLE investment account for my special needs child’s future. I would set aside $10,000 in a money market account paying interest and managing risk with liquid funds. The remaining $21,000 would be invested in a diversified ETF portfolio to maximize long-term growth potential. This approach balances family financial security, future planning, and investment growth.”

Jamie Bosse, CFP at CGN Advisors

“If I had an additional $50,000 to invest, I would allocate $10,000 to bolster my children’s 529 plans (I have four) and invest the remaining $40,000 in a brokerage account, primarily in growth-oriented index funds.

I would prioritize a brokerage account because it provides a high degree of flexibility — it isn’t subject to the restrictions of retirement accounts like IRAs, allowing access to funds at any time for any purpose.

For the brokerage account, I would choose a long-term growth index fund, as I do not anticipate needing these funds in the near future. This approach would allow me to capitalize on the potential for compound growth over time, optimizing wealth accumulation for future financial goals.”

How much money do you need to be happy?

Money influences where we choose to live, what we do for a career, and even what we eat for dinner. Having enough money frees us from issues like hunger, housing insecurity and medical debt. The primary benefit of earning more money is that it serves as a buffer when you’re hit with negative life events, says Jon Jachimowicz, a professor of business administration at Harvard University. But some researchers say Killingsworth is looking at the wrong end of the equation.

The relationship between money and happiness, though, is quite complicated.

Money influences where we choose to live, what we do for a career, and even what we eat for dinner. Having enough money frees us from issues like hunger, housing insecurity and medical debt.

The primary benefit of earning more money is that it serves as a buffer when you’re hit with negative life events, says Jon Jachimowicz, a professor of business administration at Harvard University.

“Money is not just a way that people can buy themselves happy moments; it is also a crucial tool for safety, security and stability,” said Jachimowicz. “Money can help soften the blow of bad times; a lack of money can make even benign things much more distressing and painful.”

While a previous study by Princeton’s Daniel Kahneman and Angus Deaton found that people’s sense of well-being leveled off when they made $75,000, followup research by Wharton School professor Matt Killingsworth, found there was no plateauing: People with high salaries reported higher levels of day-to-day and overall life fulfillment

Kahneman and Deaton measured happiness by asking people to share their evaluative well-being, or their measure of happiness after an event occurred.

Killingsworth examined experienced well-being, or people’s emotions as they occur. With this new metric, he determined that as income increased, people’s evaluative and experienced well-being rose accordingly.

But some researchers say Killingsworth is looking at the wrong end of the equation:

“It might be that if we worked on our mental health and burnout, we’d perform better at work,” said Laurie Santos, a psychology professor at Yale and host of the podcast The Happiness Lab. “This might lead to more positive outcomes in terms of our job success and salary.”.

There are multiple studies backing this idea that happiness and positive emotions precede higher pay, not the other way around.

Financial Planning Basics: How to Make a Plan

A financial plan is a document that shows your financial situation, goals and strategies for achieving those goals. It’s helpful to reevaluate your financial plan after major life milestones, such as getting married, starting a new job, having a child or losing a loved one. Online services like robo-advisors have also made financial planning assistance more affordable and accessible than ever. Ready to get started? See our roundup of the best financial advisors to help you plan for your financial future, and get a recommended match for your 401(k) If you have an employer-sponsored retirement plan such as a 401(K), and does your employer match any part of your contribution? You can start small — $500 is enough to cover small emergencies and repairs so that an unexpected bill doesn’t run up credit card debt. If you’re struggling with revolving debt, a debt consolidation loan or debt management plan may help you wrap several expenses into one monthly bill at a lower interest rate. It’s worth it to consider putting in to a 403(b) or similar plan that you gradually expand.

A financial plan is a document that shows your financial situation, goals and strategies for achieving those goals. A comprehensive plan can often include details about cash flow, savings, debt, investments and more.

A financial plan isn’t a static document — it’s a tool to track your progress and one you should adjust as your life evolves. It’s helpful to reevaluate your financial plan after major life milestones, such as getting married, starting a new job, having a child or losing a loved one.

You can make a financial plan yourself or get help from a financial planning professional. Online services like robo-advisors have also made financial planning assistance more affordable and accessible than ever.

» Ready to get started? See our roundup of the best financial advisors.

Advertisement 1 Answer a few simple questions 2 Get a recommended match 3 Start achieving your money goals What’s your financial priority? Financial Planning Retirement Planning Investment Management Tax Strategy Other Match with a financial advisor for free

Financial planning in 9 steps

1. Set financial goals

A good financial plan is guided by your financial goals. If you approach your financial planning from the standpoint of what your money can do for you — whether that’s buying a house or helping you retire early — you’ll make saving feel more intentional.

Make your financial goals inspirational. Ask yourself: What do I want my life to look like in five years? What about in 10 or 20 years? Do I want to own a car or a house? Do I want to be debt-free? Pay off my student loans? Are kids in the picture? How do I imagine my life in retirement?

Having concrete goals can help you identify and complete the next steps and provide a guiding light as you work to make those aims a reality.

2. Track your money

Get a sense of your monthly cash flow — what’s coming in and what’s going out. An accurate picture is key to creating a financial plan and can reveal ways to direct more to savings or debt pay-down. Seeing where your money goes can help you develop immediate, medium-term and long-term plans.

For example, developing a budget is a typical immediate plan. NerdWallet recommends the 50/30/20 budget principle: 50% of your take-home pay goes toward needs (housing, utilities, transportation and other recurring payments), 30% goes toward wants (dining out, clothing and entertainment) and 20% goes toward savings and debt repayment.

Reducing credit card or other high-interest debt is a common medium-term plan, and planning for retirement is a typical long-term plan.

3. Budget for emergencies

The bedrock of any financial plan is putting cash away for emergency expenses. You can start small — $500 is enough to cover small emergencies and repairs so that an unexpected bill doesn’t run up credit card debt. Your next goal could be $1,000, then one month’s basic living expenses, and so on.

Building credit is another way to shockproof your budget. Good credit gives you options when you need them, like the ability to get a decent rate on a car loan. It can also boost your budget by getting you cheaper rates on insurance and letting you skip utility deposits.

4. Tackle high-interest debt

A crucial step in any financial plan: Pay down high-interest debt, such as credit card balances, payday loans, title loans and rent-to-own payments. Interest rates on some of these may be so high that you end up repaying two or three times what you borrowed.

If you’re struggling with revolving debt, a debt consolidation loan or debt management plan may help you wrap several expenses into one monthly bill at a lower interest rate.

5. Plan for retirement

If you visit a financial advisor, they will be sure to ask: Do you have an employer-sponsored retirement plan such as a 401(k), and does your employer match any part of your contribution? True, 401(k) contributions decrease your take-home pay now, but it’s worth it to consider putting in enough to get the full matching amount. That match is free money.

If you have a 401(k), 403(b) or similar plan, financial advisors also generally suggest that you gradually expand your contributions toward the IRS limit: $23,500 in 2025. People age 50 and older can contribute an extra $7,500 as a catch-up contribution. Due to the Secure 2.0 Act, those ages 60, 61, 62 and 63 get a higher catch-up contribution of $11,250 .

Another savings vehicle for retirement planning is an IRA, or individual retirement arrangement. These tax-advantaged investment accounts can further build retirement savings. The contribution limit is $7,000 in 2025 ($8,000 if age 50 and older).

6. Optimize your tax planning

For many of us, taxes take center stage during filing season, but careful tax planning means looking beyond the Form 1040 you submit to the IRS each year.

For example, if you’re routinely getting a sizable refund, that may be a sign that you’re needlessly living on less throughout the year. Learning how and when to review your W-4, the form you fill out for your employer, can help you to take control of your future. Adjust your withholdings on your W-4, and you can either keep more of your paycheck or pay a smaller tax bill.

Getting cozy with the tax law also means looking into tax credits and deductions ahead of time to understand which tax breaks could make a difference when it comes time to file. The government offers many incentives for taxpayers who have children, invest in green home improvements or technologies, or are even pursuing higher education.

7. Invest to build your future goals

Investing might sound like something for rich people or for when you’re established in your career and family life. It’s not. Investing can be as simple as putting money in a 401(k) and as easy as opening a brokerage account (many have no minimum to get started). Financial plans use a variety of tools to invest for retirement, a house or college.

8. Manage risk with insurance planning

Use insurance to protect your financial stability so a sudden setback doesn’t derail you. There are insurance products to consider for almost every stage of life.

For example, renters insurance can provide affordable coverage for your belongings that pays out if they are destroyed or stolen, even if you’re just renting a room in an apartment. Once you’re ready to buy a home, homeowners insurance can cover your belongings and your house.

Life insurance protects loved ones who depend on your income. Term life insurance, covering 10-year to 30-year periods, is a good fit for most people’s needs.

9. Estate planning: Protect your financial well-being

Financial planning also means looking out for your future needs, as well as mapping things out for your loved ones. Creating a will can help ensure your assets are distributed according to your wishes. Other types of estate-planning documents can also provide your relatives with clarity on how you would like to be cared for and who should manage your affairs.

When to make a financial plan

There’s never a bad time to start financial planning, but there are a few life events that are good catalysts for making a financial plan.

Having children: Part of parenthood is figuring out how to achieve a variety of short-term and long-term financial goals, such as paying for childcare and eventually college education. A financial plan can act as a roadmap toward these goals. Plus, a 2023 study from Brigham Young University showed that parent financial literacy has a major effect on children’s financial behaviors later in life [0] View all sources Brigham Young University . What Impact Do Parents Have on Their Children’s Financial Future? . Accessed Oct 22, 2024.

A sudden increase in income or assets: A windfall, new job or major promotion may change your quality of life significantly, and a financial plan can help you avoid lifestyle creep.

Serious illness: Health problems are scary in their own right — and they can also introduce new, ongoing expenses that can make it difficult to stay financially on track. A financial plan can help you feel more confident about your ability to meet financial goals in spite of a serious illness.

Retirement: A financial plan can help you navigate life after you stop working — in particular, it can help you make your savings last longer. A 2015 study published in the CFA Institute’s Financial Analysts Journal found that a carefully planned savings withdrawal strategy can add more than three years to a portfolio’s longevity, on average [0] View all sources Financial Analysts Journal . Tax-Efficient Withdrawal Strategies . Accessed Oct 22, 2024.

How to get financial planning help

If you’re not the DIY type or simply want professional help managing some tasks and not others, you don’t have to go it alone. Consider what kind of help you need:

Complete financial plan and investment advice

Online financial planning services offer virtual access to human advisors. A basic service would include automated investment management (like you’d get from a robo-advisor), plus the ability to consult with a team of financial advisors when you have other financial questions.

More comprehensive providers basically mirror the level of service offered by traditional financial planners: You’re matched with a dedicated human financial advisor who will manage your investments, create a comprehensive financial plan for you, and do regular check-ins to see if you’re on track or need to adjust your financial plan.

» Want to work with a local advisor? Learn how to find a financial advisor near you.

Specialized guidance and/or want to meet with an advisor face-to-face

If you have a complicated financial situation or need a specialist in estate planning, tax planning or insurance, a traditional financial advisor in your area may fit the bill. To avoid conflicts of interest, consider fee-only financial advisors who are fiduciaries (meaning they’ve signed an oath to act in the client’s best interest).

Note that some traditional financial advisors decline clients who don’t have enough to invest; the definition of “enough” varies, but many advisors require $250,000 or more. If you want to know more about how much seeing an advisor will cost, read our guide to financial advisor fees.

Portfolio management only

Robo-advisors offer simplified, low-cost online investment management. Computer algorithms build an investment portfolio based on goals you set and your answers to questions about your risk tolerance. After that, the service monitors and regularly rebalances your investment mix to ensure you stay on track. Because it’s all digital, it comes at a much lower cost than hiring a human portfolio manager.

Why is financial planning important?

Financial planning can help you feel more confident about navigating bumps in the road — like, say, a recession or historic inflation. According to Charles Schwab’s 2024 Modern Wealth Survey, Americans who have a written financial plan feel more in control of their finances compared with those without a plan [0] View all sources Charles Schwab . Charles Schwab Modern Wealth Survey 2023 . Accessed Jul 12, 2024.

Once your basic needs and short-term goals have been addressed, a financial plan can also help you tackle big-picture goals. Thoughtful investing, for example, can help build generational wealth, and careful estate planning can ensure wealth gets passed down to your loved ones.

8 Ways to Get the Cheapest Car Insurance Rates

Increasing your deductible will lower your premium, but be prepared to pay more out of pocket if you file a claim. If you drive an older vehicle, you likely can drop comprehensive and collision coverage. The car insurance company that’s cheapest for one person in one place might be the most expensive option for a driver in a different state. Your insurance credit score is a significant factor in the car insurance quotes you receive except for a few states.. California, Hawaii and Massachusetts don’t allow insurers to use credit when determining car insurance rates. If your car is older and has a low market value, it may not make sense to shell out for these types of coverage. You can usually get a discount if you:Bundle car insurance with other policies, such as homeowners insurance. Insure multiple cars with one policy. Have a clean driving record. Pay your entire annual or six-month premium at once. Agree to receive documents online. Own a car with certain anti-theft or safety features.

If you drive an older vehicle, you likely can drop comprehensive and collision coverage.

To find the cheapest car insurance rates available to you, shop around with different insurers.

None of us wants to spend more than we need to for car insurance, but it isn’t always obvious how to get lower rates.

Dozens of insurance companies, large and small, are vying for your business. Many have an eye-glazing assortment of policy options, making it hard to compare policies and figure out who’s offering lower car insurance rates.

See what you could save on car insurance Easily compare personalized rates to see how much switching car insurance could save you. Zip code Get My Rates

Here are eight things you can do to ensure you get good coverage at the cheapest possible rate.

1. Don’t assume any one company is the cheapest

Some companies spend a lot of money on commercials to convince you they offer the lowest car insurance rates. But no single insurer is the low-price leader for everyone. The car insurance company that’s cheapest for one person in one place might be the most expensive option for a driver in a different state.

The only way to ensure you’re getting the lowest rate possible is to compare car insurance rates.

2. Don’t ignore local and regional insurers

Just four companies — Allstate, GEICO, Progressive and State Farm — control more than half of the nation’s auto insurance business. But smaller, regional insurers such as Auto-Owners Insurance and Erie Insurance often have higher customer satisfaction than the big names — and they may have lower car insurance rates, too.

3. Ask about discounts

Insurers typically provide car insurance discounts. While they will vary by insurance company and which state you live in, you can usually get a discount if you:

Bundle car insurance with other policies, such as homeowners insurance.

Insure multiple cars with one policy.

Have a clean driving record.

Pay your entire annual or six-month premium at once.

Agree to receive documents online.

Own a car with certain anti-theft or safety features.

Are a member of particular professional organizations or affiliate groups.

Don’t be swayed, however, by a long list of possible discounts. Compare rates from multiple insurers.

4. Work on your credit

Your insurance credit score is a significant factor in the car insurance quotes you receive except for a few states. California, Hawaii and Massachusetts don’t allow insurers to use credit when determining car insurance rates. Insurance companies say customers’ credit has been shown to correlate with their chances of filing claims.

A NerdWallet analysis found that having poor credit can increase people’s car insurance rates by hundreds of dollars a year compared with having good credit. (In most situations, a FICO score of 579 or lower is considered “poor” credit, but insurers have their own credit models that may have a different cutoff.)

Build your credit history — and get lower insurance rates — by paying your credit card bills and loan payments on time and reducing your debt. Track your progress by checking your credit score regularly.

See what you could save on car insurance Easily compare personalized rates to see how much switching car insurance could save you. Zip code Get My Rates

5. Skip comprehensive and collision coverage for an older car

Collision coverage pays to repair the damage to your vehicle from another car or an object such as a fence. Comprehensive coverage pays to repair vehicle damage from weather, animal crashes, floods, fire and vandalism. It also covers car theft. But the maximum payout under either policy is limited by the value of the car if it’s totaled or stolen. If your car is older and has a low market value, it may not make sense to shell out for these types of coverage.

6. Raise your deductible

If you buy comprehensive and collision coverage, you can save money by opting for higher deductibles. (There is no deductible on liability insurance, which pays for the damage you cause others in an accident.) But this should only be an option if you know you can afford the higher amount if you ever need to file a claim.

🤓 Nerdy Tip Compare auto insurance quotes with different comprehensive and collision deductible amounts to see how much you might save if you were to choose a higher deductible.

7. Consider usage-based or pay-per-mile insurance

If you’re a safe driver who doesn’t log many miles, consider a usage-based insurance program such as Allstate’s Drivewise, Progressive’s Snapshot or State Farm’s Drive Safe & Save. You might qualify for a discount based on driving habits like how much you drive, what time of day you drive and how well you drive.

If you truly don’t drive much at all, you could save money by switching to a pay-per-mile insurance program such as Metromile, Allstate’s Milewise or Nationwide’s SmartMiles.

Be aware that opting into a usage-based or pay-per-mile insurance program means you’re allowing your insurance company to track your driving behavior. This is typically done through either a device that plugs into your car’s diagnostic port or an app you download onto your smartphone.

8. Check insurance costs when buying a car

Source: https://www.fox6now.com/news/adequate-car-insurance-finance-professor-shares-ways-save