More employers are sending workers shopping for their own health coverage

How did your country report this? Share your view in the comments.

Diverging Reports Breakdown

More employers are sending workers shopping for their own health coverage

A small, growing number of employers are putting health insurance decisions entirely in the hands of their workers. They’re giving workers money to buy their own coverage in what’s known as Individual Coverage Health Reimbursement Arrangements, or ICHRAs. Advocates say this approach provides small companies that couldn’t afford insurance a chance to offer something. It also caps a growing expense for employers and fits conservative political goals of giving people more purchasing power over their coverage. But ICHRas place the risk for finding coverage on the employee, and they force them to do something many dislike: Shop for insurance.

Instead of offering traditional insurance, they’re giving workers money to buy their own coverage in what’s known as Individual Coverage Health Reimbursement Arrangements, or ICHRAs.

Advocates say this approach provides small companies that couldn’t afford insurance a chance to offer something. It also caps a growing expense for employers and fits conservative political goals of giving people more purchasing power over their coverage.

But ICHRAs place the risk for finding coverage on the employee, and they force them to do something many dislike: Shop for insurance.

“It’s maybe not perfect, but it’s solving a problem for a lot of people,” said Cynthia Cox, of the nonprofit KFF, which studies health care issues.

Here’s a closer look at how this approach to health insurance is evolving.

What’s an ICHRA?

Normally, U.S. employers offering health coverage will have one or two insurance options for workers through what’s known as a group plan. The employers then pick up most of the premium, or cost of coverage.

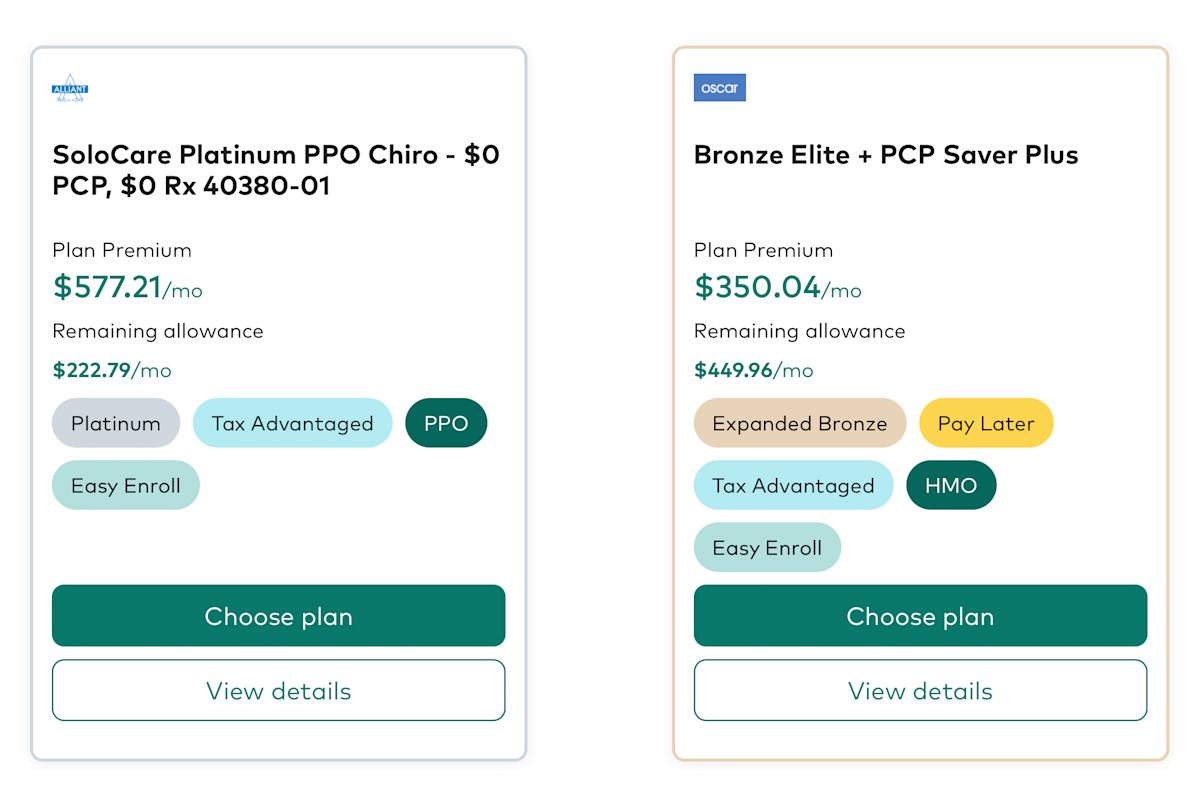

ICHRAs are different: Employers contribute to health insurance coverage, but the workers then pick their own insurance plans. The employers that use ICHRAs hire outside firms to help people make their coverage decisions.

ICHRAs were created during President Donald Trump’s first administration. Enrollment started slowly but has swelled in recent years.

What’s the big deal about ICHRAs?

They give business owners a predictable cost, and they save companies from having to make coverage decisions for employees.

“You have so many things you need to focus on as a business owner to just actually grow the business,” said Jeff Yuan, co-founder of the New York-based insurance startup Taro Health.

Small businesses, in particular, can be vulnerable to annual insurance cost spikes, especially if some employees have expensive medical conditions. But the ICHRA approach keeps the employer cost more predictable.

Yuan’s company bases its contributions on the employee’s age and how many people are covered under the plan. That means it may contribute anywhere from $400 to more than $2,000 monthly to an employee’s coverage.

How is this approach different?

ICHRAs let people pick from among dozens of options in an individual insurance market instead of just taking whatever their company offers.

That may give people a chance to find coverage more tailored to their needs. Some insurers, for instance, offer plans designed for people with diabetes.

Source: https://finance.yahoo.com/news/more-employers-sending-workers-shopping-155522822.html